RBI’s 1-hour UPI delay above ₹10000 is about to change how you send money and most people don’t know it’s coming.

You’re rushing to pay a vendor. You open your UPI app, enter ₹12,000, and hit send. But the money doesn’t move for one hour.

But the money doesn’t move for one hour.

That’s exactly what the RBI is proposing, and most people don’t understand why.

The Reserve Bank of India recently released a discussion paper outlining four safeguards for digital transactions, with the headline proposal being a one-hour delay on account-to-account transfers above ₹10000 IBTimes India covering both UPI and IMPS.

This one change could affect millions of daily transactions across India. Just like platforms are tightening their rules Instagram recently reduced its hashtag limit too regulators are now stepping into payments.

In this blog, I’ll break down:

In this blog, I’ll break down:

- What the RBI is actually proposing

- Why it’s happening now

- How it works practically

- The real tradeoffs you need to know

- What this means for regular UPI users like you

The Problem: Why UPI Is Getting “Slowed Down”

Most people assume digital payment fraud happens because of hacked systems or stolen OTPs.

That’s not the real picture anymore.

The RBI emphasised that most digital payment frauds are no longer system breaches but social-engineering scams, where users are manipulated into authorising transactions themselves. These are classified as APP (Authorised Push Payment) frauds.

In simple terms: you are tricked into sending the money yourself.

And the numbers are alarming. Fraud complaints surged from 2.6 lakh in 2021 to 28 lakh in 2025. Over the same period, the reported value of frauds grew from ₹551 crore to ₹22,931 crore.

The speed of UPI, which is its biggest strength, is also what fraudsters exploit.

What Exactly Is RBI Proposing?

This is not a final rule. It is a discussion paper with four proposals.

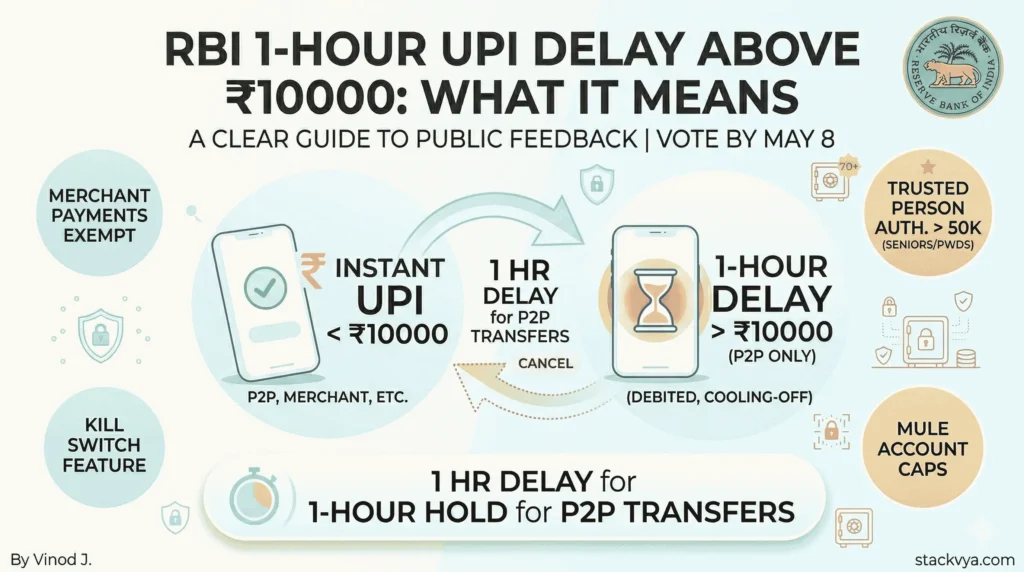

Proposal 1 — The 1-Hour Delay (The Main One)

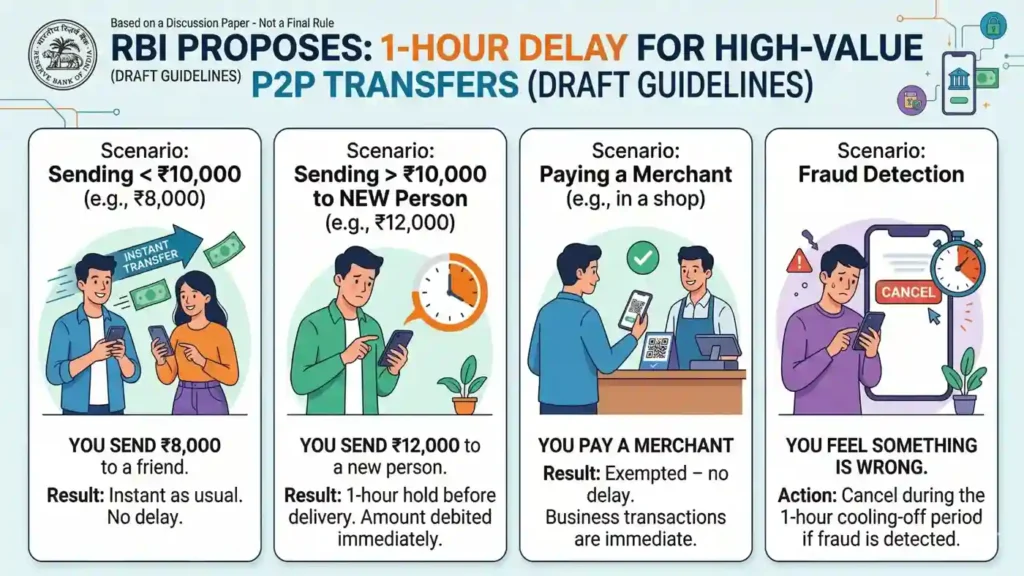

Under the draft guidelines, person-to-person (P2P) transfers above ₹10000 would be subject to a one-hour execution delay. The amount would be debited immediately but the transfer would complete only after the cooling-off period, during which users can cancel the transaction if they detect fraud.

Here’s the practical breakdown:

| Situation | What Happens |

|---|---|

| You send ₹8,000 | Instant as usual |

| You send ₹12,000 to a new person | 1-hour hold before delivery |

| You pay a merchant | Exempt no delay |

| You feel something is wrong | Cancel during the 1 hour |

Proposal 2 — Trusted Person Authentication

For payments above ₹50,000, senior citizens aged 70 and above, along with persons with disabilities, may need authorisation from a trusted contact before completing such payments.

Proposal 3 — Caps on Credits to Suspicious Accounts

Accounts flagged as potential mule accounts (used to route fraud money) could have annual credit limits imposed. Transfers beyond ₹25 lakh could face additional checks before funds are released.

Proposal 4 — The Kill Switch

Another important proposal is a quick “kill switch” feature. This option can allow users to block digital payments instantly if fraud is suspected. Analytics Insight This is already live in Singapore and being rolled out in Australia.

Why This Approach? The Psychology Behind the Delay

This is the part most news articles miss.

The delay is not just a technical speed bump. It is a psychological intervention.

Fraudsters typically rely on creating urgency and maintaining continuous psychological pressure on the victim to prevent deliberation. Introducing lag at the payer’s end breaks the fraudster’s psychological control.

Think about every scam call you’ve heard of:

- “Your account will be blocked in 1 hour!”

- “Send the money NOW or you’ll be arrested!”

- “This is your last chance!”

The moment there is a forced 60-minute pause, that pressure collapses. The victim has time to call a family member, think clearly, or simply cancel.

That is the entire logic behind this proposal.

The Real Tradeoffs (Both Sides)

This is where honest analysis matters more than just repeating the headline.

Why this could work:

While P2P transactions above ₹10000 account for roughly 45% of reported fraud incidents, they represent nearly 98.5% of the total monetary loss. India Hood The targeting is precise.

Globally, similar measures already exist. The UK payment system allows banks to delay suspicious outbound payments by up to 72 hours, while Singapore has implemented 12-hour cooling-off periods for high-risk actions.

Why some experts are cautious:

Not everyone agrees this is clean solution. As one payments expert noted, the popularity and acceptance of UPI lies in its instant nature — a blanket delay on all payments disrupts that convenience. The need of the hour is a triangulated risk scoring of transactions rather than a blanket pausing. Business Today

There are also practical concerns. What if you need to pay for an emergency medical expense? What if a vendor needs the money urgently? The ₹10000 threshold may be too low for many urban users.

The RBI also acknowledged that fraudsters may simply pressure victims into whitelisting transactions, reducing the mechanism’s effectiveness.

What Stays the Same (Important)

Before you panic about your daily UPI use:

Smaller payments will likely continue without any delay, so everyday usage will not be impacted.

Merchant payments, bill payments, e-mandates, NACH, and cheques are all proposed to be exempt from the delay. This is about person-to-person high-value transfers specifically.

What Happens Next?

This is still a proposal. The RBI has invited stakeholder comments on the proposal until May 8, after which final guidelines are expected.

If you want to share your opinion, you can submit feedback through the RBI’s Connect 2 Regulate portal before the deadline.

Key Takeaways

- The RBI 1-hour UPI delay above ₹10000 is a proposal, not a final rule yet

- It targets person-to-person transfers only — merchant payments are exempt

- The goal is to break the psychological pressure tactics used in scam calls

- There are valid concerns about convenience, especially for urgent transfers

- Additional protections for senior citizens and a “kill switch” feature are also on the table

- Public feedback deadline is May 8, 2026

Conclusion

The RBI 1-hour UPI delay above ₹10000 is not about making payments slower for the sake of it.

It is about buying you 60 minutes to think when a scammer is trying to make you act in 60 seconds.

Whether the ₹10000 threshold is right, whether a blanket delay is better than smart risk scoring — these are fair debates. But the underlying problem it is solving is very real.

Digital fraud in India has grown nearly 40x in value over four years. Something has to change.

The question is: what are you willing to trade for safety?